Putin had a dream.

And in that fever dream, he strutted into Tianjin last week declaring war on "financial neo-colonialism" at the Shanghai Cooperation Organization summit. His grand vision? A gang of dictators—one that sells oil and gas to the western world to survive, and one that sells anything and everything to the western world—would somehow conjure a parallel financial universe into existence.

No more bowing to the IMF, Putin proclaimed. The SCO would issue joint bonds, build rival institutions, and create their own payments systems. So the leader who sent his thugs to audit his central bank and a leader whose central bank is the world's most notorious currency manipulator would join hands to forge a "transparent, impartial and trustworthy" financial system.

Even GOP politicians famous around the world for spinning lalaland economic stories would find that hard to swallow.

The pitch sounds seductive on paper—who wouldn't want to dodge Washington's sanctions and shake off institutions built in 1944? But Putin's bond bonanza plan runs headlong into a brutal reality: institutional credibility cannot be decreed into existence.

When investors look at potential SCO bonds, they see a patchwork of clashing credit ratings, divergent monetary policies, and zero transparency. They see India and China glaring at each other across contested borders while Central Asian members jealously guard their sovereignty.

Would any rational investor gamble on debt issued by this alphabet soup of rivalries? Even with China shouldering the risk, an "SCO bond" would look like a Chinese instrument wearing borrowed clothes.

I've seen a lot of la-la-land economics in my time, but never on this scale. The fact that Putin even thought this was achievable reveals exactly how much he understands about financial markets. Trust—the true currency of any financial system—is the one thing the SCO, BRICS, and most Russian institutions conspicuously lack. Without it, all the grand declarations in Tianjin remain just that: empty theater.

The cruel irony is that while Putin fantasizes about financial revolution in Tianjin, he's systematically destroying the one Russian institution that actually commands international respect. If not for Elvira Nabiullina and her team at the Central Bank, Russia would have imploded long ago. Putin lucked into her—a technocrat who managed to navigate western sanctions, oil crashes, and the initial shock of his Ukrainian adventure. He was smart enough to stick with her.

But since December 2024, Putin has been steadily clipping her wings. Political audits, interference in monetary policy, pressure to fund his war machine—each intervention weakens the very institution that kept Russia's economy from complete collapse. It's economic self-sabotage on an epic scale, and frankly, I hope he keeps it up.

Because right now, Putin needs Nabiullina more than ever. He's caught in a perfect economic storm that would challenge even the most competent central banker. On one front, Ukraine's systematic campaign against Russian refineries—launched in early August and continuing relentlessly—is driving up processing costs and choking profit margins. On the other front, OPEC+ itself is flooding the market with supply, undermining Russia's own oil revenues.

The numbers tell the story: OPEC+ added 411,000 barrels per day in June and July each. Then came August's massive 555,000 bpd surge, matched again in September. November brings another 197,000 bpd boost. That's over 2.1 million additional barrels hitting global markets since June—with Russia, as an OPEC+ member, essentially voting to undercut its own war chest.

This steady supply creates the perfect buffer for Ukraine's refinery campaign. Every drone strike on Russian oil infrastructure can proceed without triggering the kind of global energy crisis that might force Western support to waver. Putin finds himself in the absurd position of participating in an oil alliance that's systematically eroding his own revenue base just when the Kremlin needs every petrodollar it can squeeze.

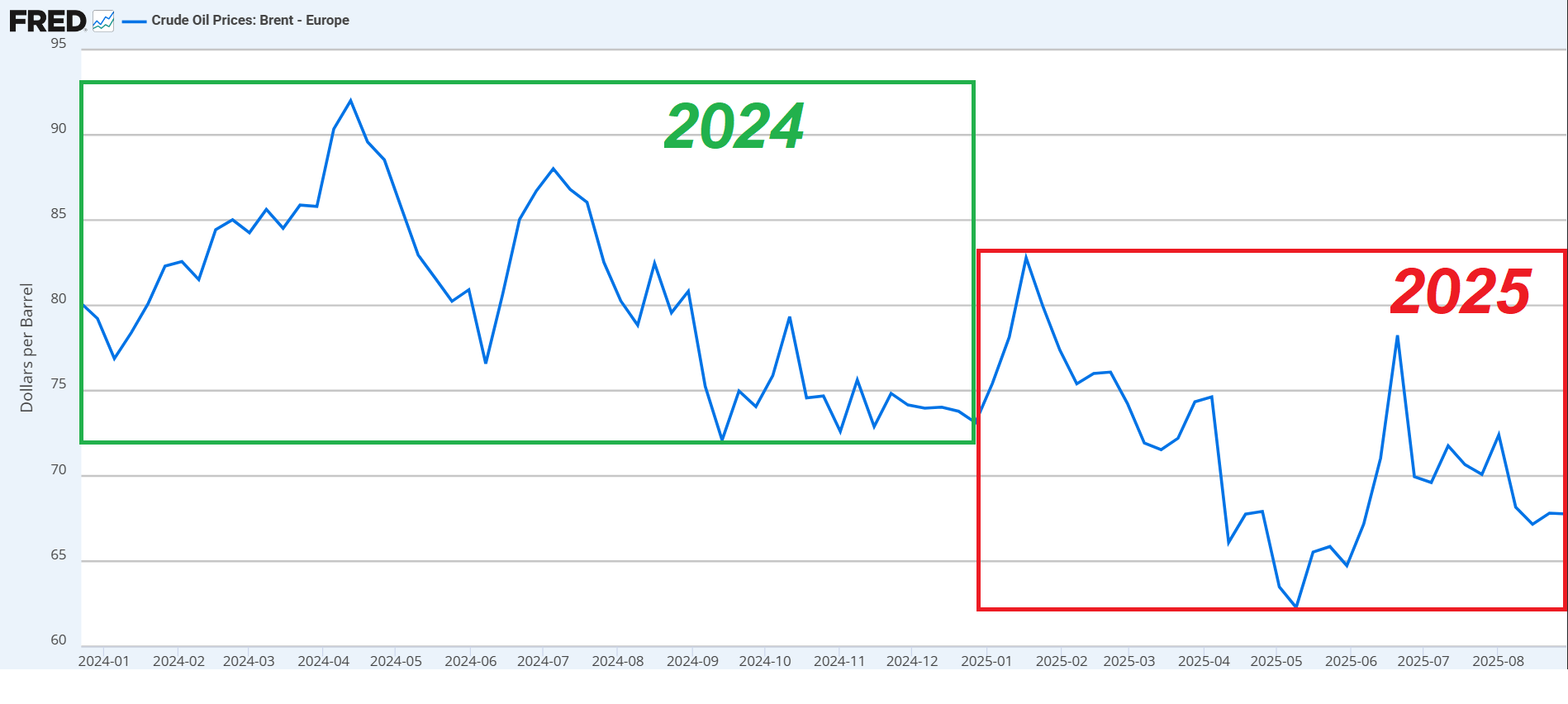

This supply bump translates directly into Putin's worst nightmare: declining oil revenues. Last year, Brent crude was trading well above the $70 mark. This year it has stubbornly remained below $70. That alone represents a drop of more than ten percent in revenue—and this rough calculation actually understates the damage, since the downward pressure on oil prices in 2025 has hammered Russian revenues by double-digit percentages.

The squeeze is forcing Putin into an impossible balancing act. He's furiously pulling back on state spending while desperately trying to maintain war expenditures. But Ukraine isn't about to let him find equilibrium. Kyiv has stayed relentlessly on the offensive against Russian refineries and oil infrastructure, turning Putin's economic crisis into a strategic vise.

Now here's where it gets interesting.

President Zelensky publicly stated they're not discussing deep strikes in Russian territory with the Pentagon.

But look at what Ukraine isn't hitting: Russia's crude oil jugular.

Ukraine possesses the firepower to demolish Russian crude oil production facilities, obliterate storage depots, and turn export terminals into smoking craters. They could systematically hunt down and destroy the entire shadow fleet—those rust-bucket tankers keeping Russian oil flowing to global markets.

If Sun Tzu were alive, he'd be screaming "what the fuck are you waiting for?"

But Ukraine's target selection tells a different story. They're laser-focused on refineries—and the pace is relentless. In just the last 36 days, Ukrainian forces have struck ten different refineries across Russian territory.

That's not random violence; that's surgical economic warfare.

Each refinery hit sends the same calculated message: we can cripple your profit margins without crashing global oil markets. Refineries process crude into high-value products like gasoline and diesel—the cash cows of the oil business. Shut down a refinery, and Russia loses the markup between crude and refined products. But the crude keeps flowing, keeping global prices stable and Western allies comfortable.

This restraint reveals sophisticated strategy.

By targeting high-margin, easily replaceable refined products while keeping hands off crude exports, they're operating under what appears to be tacit coordination with the Trump administration. The message is clear: increase Russia's war costs without triggering a global energy crisis that could fracture Western support.

I support this approach because it gives Ukraine time for the PURL scheme—which allows them to buy American weapons using European funds—to kick into high gear. After they acquire the weapons, they can then expand into other sectors of Russia's war economy, and there's plenty to choose from.

Meanwhile, Ukraine's own defense industrial base has undergone a remarkable transformation. The numbers tell the story of Ukrainian resilience: they now manufacture 60% of the weapons used on the battlefield, nearly double last year's 35%. European funding flows into Ukraine's defense industry spiked in March and then stabilized into a steady rhythm, fueling domestic production of artillery shells, howitzers, drones, and even automatic weapons.

The shift runs deeper than production numbers. Ukraine is transitioning from Soviet-designed Kalashnikovs to US-designed AR-15 assault rifles. The changeover began in 2023, and at some point the Soviet weapons will be dumped for good—a symbolic and practical break from Moscow's military legacy.

This reveals a top-down effort to build Ukrainian military independence from the ground up. This is fundamentally rewiring Ukraine's defense DNA.

As a result, Ukraine won't need to remain dependent on American weapons much longer. What they need is a specific set of weapons, with air defense and long-range missiles at the top of the list. I think $10 billion should be more than enough to tilt the table.

Consider the ERAM sales as an example: 3,350 missiles cost $840 million. Ukraine could drop 20 missiles a day for six months straight. The right weapons at volume, delivered quickly, will not only reduce procurement costs but allow Ukraine to forcefully seize control of the war inside occupied territories.

But does this mean Ukraine has won?

Not yet.

It means the tide has shifted. Ukraine is pulling ahead, but they need to maintain this trajectory. And we need to stop counting chickens before they hatch.

Russia will likely mount one massive push soon—perhaps their last roll of the dice. Ukraine faces a dual challenge: they must simultaneously plan to absorb this coming assault while preparing the counteroffensive that will follow. This isn't sequential planning; it's parallel strategic preparation.

During the Russian push, Ukraine's job is to hold the line, perhaps even punch through somewhere if opportunities arise. But the real prize comes after—when Russian forces have burned through their reserves and exhausted their offensive capacity. That's when Ukraine should strike back hard.

The window for preparing these post-wave counterattacks is now, while Russia is still gathering strength for their offensive. Ukraine must be ready to pivot from defense to offense the moment Russian momentum breaks.

If this analysis resonates with you, join thousands of readers who believe informed citizens are democracy's best defense. Subscribe to The Concis for deep-dives that mainstream media won't give you.

Let's protect the democracies, together.

“Refineries process crude into high-value products like gasoline and diesel—the cash cows of the oil business. Shut down a refinery, and Russia loses the markup between crude and refined products.”

Yes, and in addition:

* The military, including in particular its logistics —freight trains as well as trucks— runs on diesel.

* Shortages of gasoline and diesel will over time cause the civilian population in Russia to understand that economic pain is coming to them from Russia’s continuing warfare against Ukraine.

so perfectly put so beautifully written